Trusted Source for Mandi Bhav Updates

![]()

Select Mandi

Trusted Source for Mandi Bhav Updates

![]()

Select Mandi

![]() Jul 02, 2026

Jul 02, 2026

![]() by Pankaj Sihag

by Pankaj Sihag

Kisan Credit Card (KCC) Scheme Explained: Loan Benefits, Limit and Eligibility for Farmers

The Kisan Credit Card scheme gives kisaans easy access to short-term crop loans for seeds, fertilisers, irrigation, and other farm needs.

Under Budget 2025–26, the loan ceiling under the Modified Interest Subvention Scheme (MISS) was increased from ₹3 lakh to ₹5 lakh.

The standard crop loan interest rate is 7%, but timely repayment can reduce the effective rate to 4%.

Loans up to ₹2 lakh are now collateral-free from January 2025.

Tenant farmers, sharecroppers, and farmer groups can also apply under the KCC eligibility criteria.

The Kisan Credit Card scheme is a government-backed agriculture loan initiative that helps farmers get low-interest institutional credit for farming expenses.

It was introduced in August 1998 based on the recommendations of the R.V. Gupta Committee, which was constituted by the Reserve Bank of India (RBI) and the National Bank for Agriculture and Rural Development (NABARD) to look into the credit delivery system for farmers. Over the last two decades, it has become one of India’s most widely used farm credit systems.

Instead of taking separate loans before every sowing season, farmers get a revolving credit line that can be used whenever needed.

This helps cover:

Fertilisers

Pesticides

Labour

Irrigation

Post-harvest costs

Allied farming needs

The biggest benefit is that repayment is linked to harvest cycles, which makes cash flow easier for farmers.

The KCC eligibility criteria are wider.

Eligible applicants include:

Individual owner-cultivators

Joint borrowers

Tenant farmers

Sharecroppers

Cultivators with valid tenancy arrangements

Self Help Groups (SHGs)

Joint Liability Groups (JLGs)

Dairy farmers

Fishery farmers

Poultry farmers

Beekeeping farmers

Applicants are usually between 18 and 75 years old. Those over 60 may be asked to provide a co-borrower, depending on the bank's policy.

Aadhaar card

PAN card (if required)

Land records or tenancy proof

Bank account details

Crop details

Passport-size photos

Before applying, it is important to check local bank requirements.

The KCC loan limit depends on:

Landholding size

Crop type

Cost of cultivation

Input costs

Irrigation expenses

Post-harvest needs

Allied farming activities

Year 1 Limit:

Scale of finance X area cultivated

10% for post-harvest and household needs

20% for farm maintenance and crop insurance

Banks usually review the account every year.

The limit may increase by 10% annually if repayment stays regular.

|

Loan Amount |

Interest Rate |

Collateral Required |

|

Up to ₹2 lakh |

7% (can drop to 4% with prompt repayment) |

No collateral (100% security-free access) |

|

₹2 Lakh to ₹5 lakh |

7% (subject to scheme guidelines) |

Crop hypothecation (standing crop acts as security) |

|

Above ₹5 lakh |

As per individual bank policy |

Land mortgage / Third-party guarantee |

Marginal farmers may also get Flexi KCC, where banks can sanction a flexible credit limit between ₹10,000 and ₹50,000 based on landholding, crop needs, and small farm expenses.

The normal crop loan interest rate under KCC is 7% per year.

This works through:

1.5% interest subvention from the government for lending institutions

3% prompt repayment incentive (PRI) for farmers who repay on time

This can bring the effective borrowing cost down to 4%.

Important points:

Timely repayment is needed for the extra benefit

Banks may ask for Aadhaar linking for subsidy processing

Late repayment can increase the total interest cost

The Kisan Credit Card scheme supports many farming needs.

It can be used for:

Seeds

Fertilisers

Pesticides

Irrigation

Labour costs

Storage

Transport

Machinery repair

Dairy

Poultry

Fisheries

Mushroom farming

Beekeeping

This makes KCC useful across the full crop cycle.

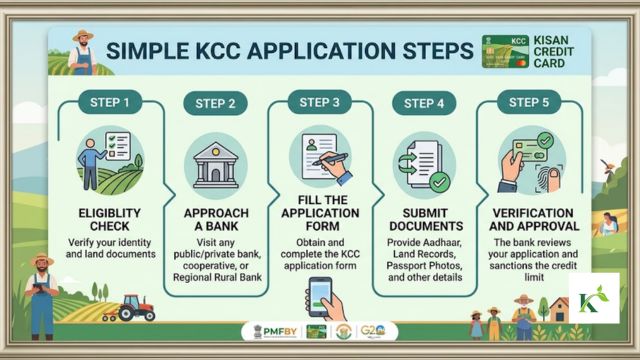

The process is simple:

Visit:

Commercial banks

Regional Rural Banks (RRBs)

Cooperative banks

Small finance banks

Common Service Centres (CSCs)

Major banks include the State Bank of India, Punjab National Bank, and Bank of Baroda, among others.

Ask for the KCC application form.

Some banks also provide online forms.

Submit:

Identity proof

Land documents

Crop details

Loan requirement details

Bank verification begins.

After approval, most banks issue a KCC debit card linked to the account.

Input costs are rising every season.

Seeds, fertilisers, labour, diesel, and irrigation all cost more now.

The Kisan Credit Card scheme gives farmers access to timely credit without depending on high-cost informal borrowing.

With:

4% effective interest

₹2 lakh collateral-free access

₹5 lakh MISS ceiling

KCC remains one of the most practical financial tools for Indian farmers.

Before every sowing season, planning your credit need can help avoid unnecessary debt pressure.

For mandi bhav, farming updates, and government scheme alerts, keep checking KhetiKisaan.

Yes. Tenant farmers and sharecroppers can apply with valid cultivation proof.

Usually 5 years, with an annual review.

You may lose the prompt repayment incentive, and your interest cost may increase.

Yes. KCC covers allied sectors like dairy, fisheries, poultry, and beekeeping.

Yes. Most KCC accounts are issued as RuPay debit cards, which can be used at ATMs and micro-ATMs.